Roberts Insurance Group Blog |

Can you get special perks insuring your home with the Roberts Insurance Group?-- The answer is YES, YOU CAN!

We all see and hear insurance companies advertise special perks or special features that are available for home insurance. But what are they? Do all companies offer them? We're going to go over some special features available for home insurance policies in Georgia. Not all companies have extra features available BUT, here at the Roberts Insurance Group, we have an extensive network of companies that DO offer special perks, which give our clients access to the very best coverage that is specifically catered to each individual household. Claim Forgiveness This special feature can be added at the beginning of the policy and apply right away or it can be something you accumulate over the years. For instance, some carriers will allow us to write the policy with a special endorsement that will go into effect day 1. So if you start a policy on Monday and have a claim Tuesday, that claim will not result in a surcharge or increased claim rating at renewal. On the other hand, some carriers have features built into the policy where they will forgive a claim after you go so many years without filing one, typically 5 years. Claim Free Discount Much like the claim forgiveness feature, this can be something that is applied at the start of the policy or after you've have been with the company for a certain amount of years (typically 3) without a claim. If it is added at the beginning of a policy, then the company is giving you credit for going a certain amount of years prior to the start without filing a claim. Decreasing Deductible Many companies offer a decreasing deductible feature that will lower your deductible by $100 or so each year you do not file a claim. We have found that many clients prefer to carry a higher deductible, meaning they pay a lower premium to the insurance company in exchange for a larger out of pocket co when they file a claim. Adding the decreasing deductible feature gives them the best of both worlds. They get a lower premium now and, assuming they do not file a claim in the first few years, a lower out of pocket down the road when they need to use their insurance. Give us a call at 678-250-8133 to see what perks and features are available for you so that you can get the very best value on your home insurance! The Roberts Insurance Group is a Georgia Insurance Broker specializing in commercial and personal insurance for our clients throughout the state of Georgia. We help our clients lower their cost of insurance with our superior claim and risk management expertise and our extensive carrier access. We are in the business of building relationships with our clients to help them grow and succeed. Contact us today to see what we can do for your family or business.

0 Comments

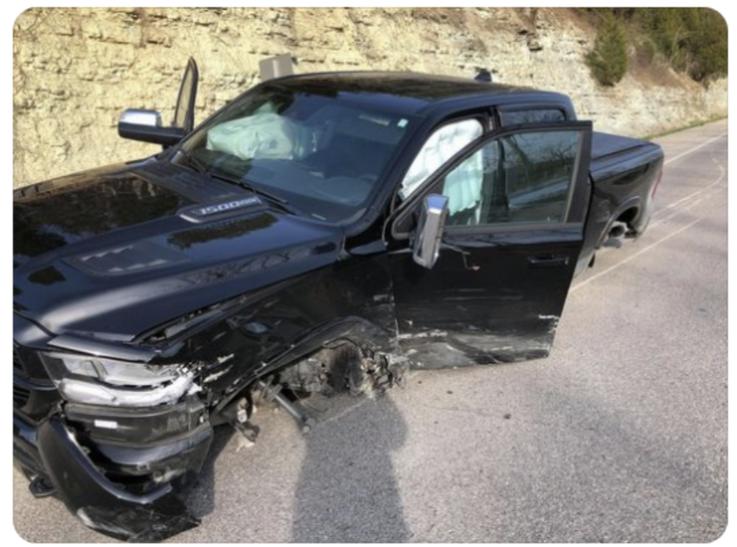

One of the BIGGEST misconceptions by Georgia drivers is that having "full coverage" means that they will be fully covered in the event of an accident. This is dangerous and could leave you, your family, or your business exposed and subject to hundreds of thousands of dollars in unforeseen costs in the event of an accident. The truth is, there's no such thing as full coverage. Now, when someone tells me they have full coverage, I do know what they mean by that. "Full coverage" typically means that someone carries comprehensive and collision coverage on their auto policy. These are the coverages used to fix or replace your vehicle if it is damaged and there is not another at-fault party. These are the coverages required if you are financing or leasing a vehicle. So why is there no such thing as full coverage? Even if you have "full coverage" you are still going to be subject to deductibles and the limitations on your policy. For example, if you have a $500 collision deductible, you're going to be responsible for the first $500 in damages to your vehicle before your auto insurance policy will begin to pay out. Also, if you have an accident and there's $100,000 in property damage and you only have $25,000 in property damage liability, your policy will pay out the $25,000 property damage liability limit and you would be responsible for the remaining $75,000. These are just 2 examples. How is having "full coverage" dangerous? This can best be explained by an experience that happened to a friend of mine. We'll call him Joe. One afternoon, Joe and his wife Sarah were driving home from lunch. On the way home, another driver veered into their lane and hit them head on. Thankfully, all parties involved were OK aside from a little soreness. What was not OK was Joe's new Ram pick up truck. The picture here is an actual picture of Joe's truck at the accident scene. Joe bought the truck brand new and had only had it for a few months. It was valued at the time of loss of around $65,000. The truck was deemed a total loss. The at-fault driver thought all was well because he had "full coverage". Little did he know that he had the Georgia state minimum liability limit requirements, which only provides $25,000 of property damage liability. The at-fault driver's insurance company paid the $25,000 with ease, leaving him a remaining balance of $40,000 owed to Joe and Sarah. Where did he come up with the $40,000? He didn't. What happened was, Joe and Sarah had to file an underinsured motorist claim on their personal auto policy to cover the difference in what was paid by the at-fault driver's policy and what the truck was valued at. After all, insurance is designed to indemnify you or make you whole again. Joe and Sarah's policy paid the remaining $40,000 with ease because Joe was correctly insured. Joe and Sarah went out and got a new truck the next day. So what happened to the at-fault driver? Joe and Sarah's insurance company took him to court and sued him for the $40,000 they had to pay as the result of him being underinsured. The at-fault driver, not having an extra $40,000 laying around, ended up having a judgment against him in the amount of $785 being garnished from his paycheck until the debt is repaid. This is almost as much as his monthly mortgage payment. So, in essence, he is not stuck having to pay the equivalent of TWO mortgage payments every month for the next 4 and a half years! Can you imagine what his life would be like if Joe and Sarah were hurt or killed in the accident? If they had hundreds of thousands of dollars in medical expenses and lost wages? This at-fault driver would be getting far more garnished from his paycheck for a MUCH longer period of time. So what is the moral of the story? The moral of the story is that, even if you have "full coverage" you're not fully covered. Even if you have $5,000,000 of liability insurance connected to your personal auto policy, you'll still be stuck having to pay out of pocket for everything over the limits in your policy. Your policy has limits that WILL NOT be exceeded. This is why it is important to review your coverage with your agent to make sure you have the right coverage. The Roberts Insurance Group is a Georgia Insurance Broker specializing in commercial and personal insurance for our clients throughout the state of Georgia. We help our clients lower their cost of insurance with our superior claim and risk management expertise and our extensive carrier access. We are in the business of building relationships with our clients to help them grow and succeed. Contact us today to see what we can do for your family or business.  When it comes to auto insurance in Georgia, there is not a one-size-fits-all solution. Every household is going to be a little different, so it's important to make sure your auto insurance policy is tailored to your unique situation. In this article, we're going to highlight 5 important coverages that Georgia drivers need to review to make sure they're properly covered in the event of a loss:

#1 Liability Limits This is arguably the most important coverage on a personal auto insurance policy in Georgia. It is also where there will be the biggest differences from household to household. The liability limits on your personal auto policy is what will be paid to the not-at-fault party in the event you are at fault for an accident. The reason this coverage is so important for Georgia drivers is because it protects your income and assets from being seized or garnished in the event you are liable for an auto accident. In Georgia, the state minimum liability limits required to drive on the roads here is $25,000/$50,000/$25,000. What do these numbers mean? The first number is the limit of insurance available for bodily injury liability per person. Simply put, if you are at fault for an accident and someone else is injured, the insurance company will pay up to $25,000 per person for the victim(s) medical bills, lost wages, pain and suffering, etc. The second number, $50,000, is the limit of bodily injury liability that would be paid out in any single accident. So if you're at fault for an accident and there are multiple people injured, the max this policy would pay out is a combined $50,000 for bodily injury. The last number, $25,000, is the amount of property damage liability that the policy would pay out. If you're at fault for an accident, your insurance company would pay up to $25,000 to fix/replace the not-at-fault party's vehicle. If you couldn't already tell, the state minimum coverage is not going to be sufficient for many accidents and would leave most Georgia residents vulnerable. There are so many cars on the roads nowadays that are worth far more than $25,000. In addition, the cost of medical care has been increasing significantly year after year. Even a short hospital stay would result in over $25,000 in medical bills. What Liability Limits Are Available For Georgia Auto Policies? Many companies will allow you to tailor each individual limit to design the policy coverage just the way you want. Some companies have a limited selection available. To keep things simple, below is a general list of alternative liability limit options you can consider: $50,000/$100,000/$50,000 $100,000/$300,000/$100,000 $250,000/$500,000/$100,000 $500,000/$500,000/$100,000 For most homeowners in Georgia, we will recommend carrying at least $100,000/$300,000/$100,000 for your liability limits. This will protect your personal finances, income, and assets from almost all at-fault accident scenarios. #2 Comprehensive and Collision Coverage Carrying comprehensive and collision coverage is what most folks consider "full coverage" these days and what you're require to carry if you are leasing or financing your vehicle. Comprehensive coverage pays to fix or replace your vehicle if it is damaged and you or another driver is not at fault for the damage. Common claims include if your car is stolen, an object falls on it, you hit an animal in the road, and glass breakage. Collision on the other hand is used when you're at-fault for the damage to your vehicle. Whether you car an accident with another vehicle or back into a stationary object. If you're at-fault for the damage, collision coverage is what will be used to fix or replace your vehicle. For most auto policies in Georgia, these claims are settled on what's called an "actual cash value" basis. Meaning that your car's value will be based on the characteristics at the time of the accident, including depreciation. #3 Medical Payments Coverage Medical payments coverage on auto policies in Georgia is used to help pay for medical expenses stemming from auto accident injuries. This coverage will typically supplement your major medical health plan and help pay for out of pocket costs you may incur following an auto accident injury. Things like co-pays, costs to meet your deductible, and things that may not be covered by your health insurance policy (like chiropractic care). We recommend reviewing your health insurance plan to help determine how much medical payments coverage you should carry. #4 Uninsured Motorist Coverage Uninsured or underinsured motorist coverage is used when you're in an accident and the other driver does not have insured OR if they don"t have enough insurance. The limits from uninsured motorist coverage will typically mirror the liability limits. You can not have more uninsured motorist coverage than liability on an auto policy in Georgia, but you can have less. There are too many drivers on the roads in Georgia who either don't have insurance or who have state minimum coverage. If you're in an accident with one of these folks, there is a really good chance you're going to need to use your uninsured/underinsured motorist coverage. In addition to reviewing your limits, you need to review what type of uninsured motorist coverage you have. There are 2 options- Excess or add-on uninsured motorist coverage and reduced uninsured motorist coverage. The best coverage option will be add-on uninsured motorist coverage. Add-on coverage means that your policy will "add-on" or stack on top of what you're able to recover from the at-fault party's policy. Reduced coverage means that your uninsured motorist limits will be reduced by what you're able to recover from the at-fault party's policy. #5 Rental Car Reimbursement If you don't have an extra vehicle to drive for a few weeks in the event your vehicle is in the shop due to a claim, you need to make sure to include rental car coverage on your Georgia auto policy. This coverage is very inexpensive and will pay for the cost of a rental car in the event your car is inoperable for a period of time following an accident. One thing to consider here is that you will need to tailor your limits to make sure you have enough coverage to get a comparable rental vehicle. For example, if you typically drive a new, $100,000 SUV or a large pick up truck, you would want to make sure your policy has enough coverage so that you can rent a similar vehicle, so the minimum coverage here would no be sufficient. If you're unsure of what coverage options or limits you and your family need, we highly recommend reviewing your situation with your agent or broker or giving us a call. We'd love to take a few minutes to make sure you're properly covered. The Roberts Insurance Group is a Georgia Insurance Broker specializing in commercial and personal insurance for our clients throughout the state of Georgia. We help our clients lower their cost of insurance with our superior claim and risk management expertise and our extensive carrier access. We are in the business of building relationships with our clients to help them grow and succeed. Contact us today to see what we can do for your family or business.  The popularity of home based businesses has been on the rise throughout Georgia over the past several years. Although running your business from your home can be a smart, cost saving decision, it can create costly gaps in your insurance coverage.

If you’re working at home you need to review your coverage ASAP. Your homeowners insurance probably doesn’t cover your business. A typical Georgia homeowner’s policy provides only $2,500 coverage for business equipment which is usually not enough to cover all of the business property you use in your business. You also need coverage for liability and business interruption. To insure your home-based business, you have three choices-endorsements to the home insurance policy, an in-home business insurance policy or a small business owner’s package insurance policy. 1) ENDORSEMENTS TO YOU CURRENT HOMEOWNERS INSURANCE POLICY Depending on the type of business you operate, you may be able to add an endorsement to your existing homeowner’s insurance policy. For as little as $14 a year in Georgia, you can double your standard homeowner’s insurance policy limits for business equipment from $2,500 to $5,000. Some companies have begun offering endorsement that includes business property insurance and limited business liability insurance coverage. 2) IN-HOME BUSINESS INSURANCE POLICY The insurance industry has responded to the growing number of home-based business by creating in-home business insurance policies. In Georgia, for under $200 per year in most cases, you can insure your business property for $10,000. General liability insurance coverage is also included in the policy. A business owner in Georgia can purchase anywhere from $300,000 to $1 million worth of liability insurance coverage. The cost of the liability coverage will depend on the amount purchased. If your business is unable to operate because of damage to your house, your in-home business policy will cover lost income and ongoing expenses such as payroll for up to one year. The policy also provides limited coverage for loss of valuable papers and records, accounts receivable, off-site business property and use of equipment. In some cases, the companies that offer these polices require that you purchase your homeowner’s and auto policies from them. 3) BUSINESS OWNER’S PACKAGE INSURANCE POLICY (BOP) Created specifically for small business, this policy is an excellent solution if your home-based business operates in more than one location or manufactured products outside the workplace. A BOP, like the in-home business policy, covers business property and equipment, loss of income and extra expenses, and liability. However, these coverage’s are on a much broader scale than the in-home business policy. 4) AUTOMOBILE INSURANCE COVERAGE If you are using your automobile for business activities-transporting supplies or products or visiting customers-you need to make certain that your automobile insurance will protect you from accidents which may occur while on business. Most personal auto insurance policies in Georgia either have exclusions or limitations to coverage when engaging in certain business activities, such as delivering goods. Please check with your insurance agent immediately to verify your insurance coverage. The last thing you want to happen is to get into an accident while delivering your products and find out that your insurance policy has an exclusion for deliver of goods, leaving you uncovered and personally responsible for paying for the accident damages. In order to get insurance coverage that will not overlap with your homeowner’s policy or leave any exposures, you should consult with an insurance professional with experience in this field. The Roberts Insurance Group is a Georgia Insurance Broker specializing in commercial and personal insurance for our clients throughout the state of Georgia. We help our clients lower their cost of insurance with our superior claim and risk management expertise and our extensive carrier access. We are in the business of building relationships with our clients to help them grow and succeed. Contact us today to see what we can do for your family or business.  Weathering a global pandemic over the last year and an epic winter storm last month seems a tall order. The upcoming spring storms in Georgia will arrive soon enough.

Yes, spring storm season brings a bit of dread. It is possible to see hailstones the size of softballs here in Georgia. Who knows what the hail and wind storms will bring? Some years have proved benign. Others have proved off-the-chart in damage and roofing claims. It doesn't hurt to plan ahead and think through what a roofing insurance claim will look like in the event your roof is severely pelted by hail or if you suffer damage from high winds. Knowing what your insurance carrier will cover as stated in your home insurance policy will help you not to have to ask, "Why won't my home insurance coverage replace my roof?" Do You Have Partial or Full Replacement Coverage? One way insurance carriers entice Georgia homeowners to contract their policy with them is to keep the insurance premium down by offering certain options which may help the pocketbook initially, but could hurt at claim time. What once was a rather straightforward process (your roof is damaged, the insurance carrier covers the full cost of replacing your roof minus your deductible) isn't always the case. We can thank "creative" dealings between roofing companies and consumers for leading insurance carriers to tighten down the standards on paying claims and increasing deductible amounts. Roofing companies offering to help customers "eat the deductible" has proven more costly and wound up hurting more than helping in the form of higher premiums. It's also illegal. As a further way to minimize cost for the insurance carrier, they have provided new solutions meant to have less of a payout to the policy owner, mainly you. One way of doing this is through a Roof Payment Schedule, a.k.a, a Depreciation Schedule. If you have this type of provision in your policy, you may not have the protection you need if your roof is altered by ice balls dropping from the sky. There are good surprises and bad surprises in life. We don't want our clients experiencing a bad surprise in learning what they though they had for coverage is just that . . . a thought. We advise knowing the difference between replacement cost and actual cash value. In this case, if you want to answer "Will my insurance coverage replace my roof?" in the affirmative, paying more in premium to do so and bypassing the savings in favor of a costlier claim experience is the route to take. Getting Covered Before the Storms If you have any doubt about your policy or know you are not covered, there is time to talk about it and most importantly, do something about it. As a local, independent insurance agent living and working right here in the Canton/Metro Atlanta area, we know this hail that will come knocking soon. We also have access to great options with carriers that pay claims consistently and promptly. We hope the right policy with the right carrier will give you the peace of mind of knowing you're covered while listening to the pounding up top. The Roberts Insurance Group is a Georgia Insurance Broker specializing in commercial and personal insurance for our clients throughout the state of Georgia. We help our clients lower their cost of insurance with our superior claim and risk management expertise and our extensive carrier access. We are in the business of building relationships with our clients to help them grow and succeed. Contact us today to see what we can do for your family or business.  As a business owner in Georgia, it is more important now more than ever to make sure your business auto insurance policy has the right coverage limits, endorsements, and symbols to not only make sure your business is properly protected-- but to make sure you aren't paying more than you need to. Million dollar liability claims are becoming the norm for auto accident liability lawsuits, which in turn is driving premiums up for business owner on their commercial auto policies.

Due to the rise in high dollar claims and high dollar premiums, we wanted to review the commercial auto insurance symbols so that Georgia business owners can review their policies to make sure their operations are properly covered and that they aren't paying for anything they don't need: Part 1- Commercial Auto Liability Symbols

Part 2- Physical Damage Coverage Symbols

As a Georgia business owner, it is important to note that sometimes you will engage in contracts that requires you to purchase coverage that is not applicable to your business OR you may enter into contracts that require less than what your business actually needs. This is very common with contractors in Georgia and is one of the main reasons it is important to review your business coverage needs and provide contract requirements to your independent insurance broker. The Roberts Insurance Group is a Georgia Insurance Broker specializing in commercial and personal insurance for our clients throughout the state of Georgia. We help our clients lower their cost of insurance with our superior claim and risk management expertise and our extensive carrier access. We are in the business of building relationships with our clients to help them grow and succeed. Contact us today to see what we can do for your family or business.  Georgia homeowners are always asking, "am I covered for water damage"? In light of a huge influx of water damage claims over the past few weeks stemming from the severe winter weather in Texas and other states, we thought it would be a good idea to go ahead and clear this up for Georgia homeowners.

The answer: sometimes. Of course with insurance, it can never be too easy or cut and dry. There are some cases where water damage is never covered. There are some cases where water damage is almost always covered. And then there are some cases where it will depend on the circumstances and the policy contract language. Let's look at each of these scenarios: When is water damage NEVER covered on a Georgia homeowners policy? Water damage will never be covered if the water is coming from the ground. If it is coming from the ground, it is considered flood water and would only be covered by a flood policy. In some states, some specialty carriers have added an endorsement for this but, as of now, there's not a Georgia home insurance policy that will cover flood damage or damage from ground water. Even if you're not in a flood plain, your home can still get damage from ground water. How you might ask? Over the years, we've seen several claims that were subsequently denied due to the damage coming from ground water. In a few instances, rain water was being redirected by down spouts to run up against the side of the home and foundation. Over time, this will allow water to seep through and begin causing damage to the interior of your home. In other instances, cracks in the basement foundation of homes has caused water to be able to seep through. This is one of the reasons you may want to consider getting a flood insurance policy to help protect your home in Georgia. When is water damage ALMOST always covered? If an outside force causes sudden and accidental damage to your home to allow rain water to leak through or if the sudden and accidental damage results in a broken pipe. Unless you have a poorly written home insurance policy with specific exclusions, damage like this will almost always be covered by your Georgia home insurance policy. Another instance where water damage is almost always covered is when there is an accident. For example, you're filling up the bathtub, you run downstairs to get something while the water is running. You get distracted and next thing you know there's water coming through the ceiling. Unintentional accidents like this are almost always going to be a covered loss. When is water damage sometimes covered? Water damage has potential to be covered by a Georgia homeowners policy when the loss is due to freezing and unfreezing (weather). Most Georgia home policies state that this is covered as long as the insured has made an effort to maintain heat inside the home. If you go out of town and turn the heat off in the dead of winter, this might not be covered. But generally speaking, as long as you keep the heat on, this should be a covered loss. Another situation that has potential for coverage is when there is a small leak that goes unnoticed. This will boil down to the policy language and the company you have your home insurance with. Some companies specifically exclude this type of leak. Others will cover this as long as the damage is addressed as soon as it is noticed. It is very important for you to read your policy, however boring it may be, to see if this is something that would be covered on your Georgia home insurance policy. The Roberts Insurance Group is a Georgia Insurance Broker specializing in commercial and personal insurance for our clients throughout the state of Georgia. We help our clients lower their cost of insurance with our superior claim and risk management expertise and our extensive carrier access. We are in the business of building relationships with our clients to help them grow and succeed. Contact us today to see what we can do for your family or business.  Things change, times change, vendors change, operations change, government requirements change, client expectations change. So ask yourself, how are things different today in your business and are your insurance policies right for the circumstances you’re in today?

Failing to review your business insurance can put everything you’ve worked so hard to build at risk. With all of that in mind, here are eight questions Georgia business owners need to ask as you approach your policy renewal date: 1. If your business has added staff, added office space or operations, congratulations! Now let’s talk about what additional or special coverages you might need at renewal. Don’t leave yourself uninsured or under-insured. Insurance carriers consider company size, revenue and funding among a long list of factors when quoting your premium. So if you’ve grown rapidly in the past year (again, congrats!) don’t be surprised if your insurance costs increase. 2. Have you entered into a joint venture, partnership or LLCs? As you grow your business, new exposures develop, so, again, a good reason to make sure coverage is properly adjusted at renewal. 3. Has your insurance carrier performed a risk control survey of your company’s operations and issued formal safety or loss prevention recommendations? Be sure you have addressed these issues and documented your compliance. 4. Do you have coverage to help carry you through the period following a fire or other loss, when you may not receive income from your customers? Business income insurance bridges that gap to help you pay bills and key employees until you are able to reopen. 5. Have you reviewed loss runs with your agent to confirm your claim records are correct and updated? Be sure that any conditions that caused claims have been addressed and solutions have been forwarded to the carrier for underwriting consideration at renewal. 6. Do you rely on networks, computers, and electronic data to conduct business? Do you handle or store sensitive customer data? Traditional coverage forms, including Property, General Liability, Crime and Errors & Omissions, typically do not adequately cover the information and network security risks of modern business operations. You may need to consider purchasing cyber or data breach coverage. 7. Do you have strong safety programs and risk management oversight? If you believe in your risk management and safety programs, then accepting higher deductibles could yield premium savings. 8. Do you have the right coverage in the event a customer sues? Even if you are not at fault, defending your reputation still will cost money. For example, General Liability does not cover claims arising out of the delivery of professional services. To address those exposures, talk to your agent about Professional Liability. Finally, while it may seem like a lot of trouble, the best commercial insurance brokers will be able to work through renewal with you fairly painlessly. That’s why renewal also is a good time to evaluate whether your broker is a good fit. If the process feels a lot like filling out college apps by yourself — overwhelming, complicated, and frustrating — it might be time to shop for a new broker. The Roberts Insurance Group is a Georgia Insurance Broker specializing in commercial and personal insurance for our clients throughout the state of Georgia. We help our clients lower their cost of insurance with our superior claim and risk management expertise and our extensive carrier access. We are in the business of building relationships with our clients to help them grow and succeed. Contact us today to see what we can do for your business.  When contractors have a loss to their equipment, it can put their entire business in jeopardy. For example, when a warehouse fire destroys all of the business' equipment, it will take some time to file a claim and acquire new equipment. Even if the claim is processed quickly, what if the equipment is back ordered? It's safe to say the current jobs/contracts are going to be at risk, along with upcoming jobs and projects. This is why it is crucial for Georgia contractors to have Business Interruption Insurance.

Choosing a BII coverage limit can be challenging with many loss variables involved. It’s important to get enough coverage to bridge potential income interruptions. Here are 10 key questions contractors should ask when considering what BII limit they need:

Taking the time to run through these scenarios and calculate the potential loss exposure can pay huge dividends down the road. In fact, it can make the difference between protecting your profits and filing for bankruptcy. How would your business fare if you were unable to operate for a week? A month? A few months? You get the picture. Since business interruption insurance is among the least understood coverage types, many contractors simply don’t have enough coverage – and that’s one of the biggest causes of business failure following a fire or other disaster. If you or a crucial supplier suffered a fire or other disaster, would your income be in jeopardy? For more information about protecting your profits with business interruption insurance, talk to the construction insurance specialists at the Roberts Insurance Group today. The Roberts Insurance Group is a Georgia Insurance Broker specializing in commercial and personal insurance for our clients throughout the state of Georgia. We help our clients lower their cost of insurance with our superior claim and risk management expertise and our extensive carrier access. We are in the business of building relationships with our clients to help them grow and succeed. Contact us today to see what we can do for your business.  According to government statistics, there are approximately 3 million work-related illnesses and injuries reported every year, or approximately 2.9 cases per 100 full-time employees. Benefit payments totaled nearly $62 billion for the most recent year in which figures were available.

Construction, as you might imagine, sees its fair share of work-related injuries but so does manufacturing, the retail sector and even finance and insurance, among others. So, what are some of the do’s and don’ts for employers and injured workers considering filing a workers’ compensation claim? Let’s start with employers:

Here, too, are a few do’s and don’ts that, if you’re an employer, you can share with your workers:

The Roberts Insurance Group is a Georgia Insurance Broker specializing in commercial and personal insurance for our clients throughout the state of Georgia. We help our clients lower their cost of insurance with our superior claim and risk management expertise and our extensive carrier access. We are in the business of building relationships with our clients to help them grow and succeed. Contact us today to see what we can do for your business. |

Contact Us(678) 250-8133 Archives

February 2022

Categories |

RSS Feed

RSS Feed